- Solutions

ENTERPRISE SOLUTIONS

Infuse new product development with real-time intelligenceEnable the continuous optimization of direct materials sourcingOptimize quote responses to increase margins.DIGITAL CUSTOMER ENGAGEMENT

Drive your procurement strategy with predictive commodity forecasts.Gain visibility into design and sourcing activity on a global scale.Reach a worldwide network of electronics industry professionals.SOLUTIONS FOR

Smarter decisions start with a better BOMRethink your approach to strategic sourcingExecute powerful strategies faster than ever - Industries

Compare your last six months of component costs to market and contracted pricing.

- Platform

- Why Supplyframe

- Resources

The electronics supply chain has made significant progress in 2024, with massive global electronic component inventory levels normalizing and supply-demand balance across most commodities contributing to more stable market dynamics.

Returning to a more balanced supply and demand situation for component procurement teams in the second half of this year and into 2025 brings benefits and drawbacks. They see more favorable supply conditions and pricing as inflation moderates and major central banks pivot strategies from lowering inflation to promoting economic growth. Conversely, buyers are experiencing less price flexibility and increases, as well as supply constraints for some electronic components and solid-state storage.

Nearly three-quarters of all Commodity IQ electronic component pricing dimensions for the second half of 2024 will be either stable, flexible, or declining. The picture improves considerably by excluding memory and storage devices, with just 6% of H2 2024 pricing characterized as rising or inflexible compared to 28% with those commodities included in the analysis.

Similarly, on the supply side, H2 2024 will conclude with 52% of all component lead times contracting with no constraints, dramatically improving to 90% without considering memory and storage. Similarly, on the supply side, H2 2024 will conclude with 52% of all component lead times contracting with no constraints, dramatically improving to 90% without considering memory and storage.

(No) Thanks for the Memories

Across all memory types, the Commodity IQ Price Index averaged 2.5 times the index baseline through the first eight months of the year, climbing 56% above the same period in 2023. This growth was primarily driven by continuously rising pricing for DRAM, particularly the high-bandwidth memory (HBM) DRAM required for data center accelerator chips, including GPUs from NVIDIA and AMD.

The leading HBM manufacturers—SK Hynix, Samsung, and Micron—have announced that all supplies are fully allocated through 2025 and likely into 2026. The severe HBM shortage impacts all geographies and end markets beyond high-performance computing, requiring long-term commitments and extended buyer demand forecasts.

With memory manufacturers shifting production capacity to HBM and DDR5 DRAM, availability and contract pricing trends for legacy DRAM variants, including DDR3 and DDR4, have turned sour for many buyers. Samsung ceased DDR3 production in Q2, and SK Hynix and Micron pivoted more capacity to HBM and DDR5.

NAND Flash memory pricing continues to swell as inventory digestion in the server market is completed, and AI applications and enterprise servers boost demand for high-capacity storage. After rising between 15% and 20% in Q2, average selling price increases by as much as 10% will be recorded for Q3.

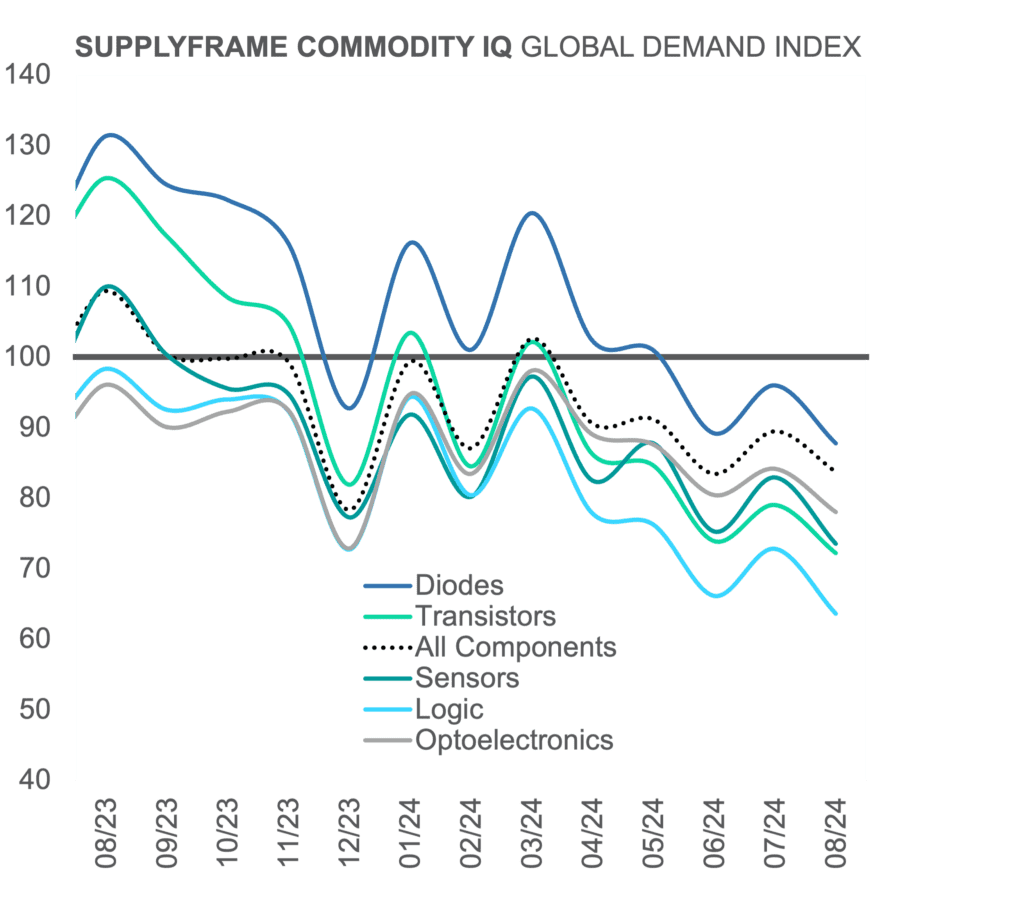

Disquieting Demand

Signaling contraction, the Commodity IQ Demand Index for all electronic components has remained below the index baseline for five consecutive months and was down 23% year-over-year for August. Across all regions, demand growth returned sequentially in July but was short-lived for Asia-Pacific and Europe-Middle East-Africa, which fell 6% and 23% in August.

The forecast for a Q3 index decline is wide-ranging, affecting nearly all component categories, including analog and digital semiconductors, passives, and interconnects. Moreover, sourcing actions for all but three commodities experienced sequential monthly declines in August.

With component manufacturer book-to-bill ratios hovering near 1:1 and 90% of lead time dimensions (excluding memory and storage devices) forecast to ebb through the second half of the year, component producers are adjusting capacities to align with still-muted demand. Yet, component manufacturers have demand growth expectations for Q4, indicating broad demand expansions in H1 2025.

What is becoming a softer peak season than expected and select end markets still struggling warrant cautious optimism. Subsequently, the Commodity IQ Demand Index forecast for Q4 is a 5% decline across all electronic components. Year-on-year through August, the Commodity IQ Design Index, as a leading indicator of demand, rose markedly by 11%.

According to multiple market researchers, smartphone shipments are expected to grow by 5% to 6% this year after two years of declines. PC shipments have risen for two consecutive quarters with all the hoopla of AI-enabled PCs and the more down-to-earth corporate upgrade shipment growth gaining momentum. Still, shipments for the full year 2024 will be at most double-digit percentage growth.

Today, some 7,000 data centers are in operation or in various stages of completion worldwide, almost double the number in 2015. There are so many that power grids can only satisfy electricity demand in some areas. In 2024, servers will represent about 20% of the global semiconductor market revenue by employing upward of 14 billion semiconductors.

Servers, AI-equipped PCs, and AI smartphones are expected to experience sales acceleration into Q1 2025, further fueling the prospect of demand recovery for passive, semiconductor, and interconnect parts in H125. This is supported by the revised World Semiconductor Trade Statistics (WSTS) global semiconductor market forecast, which calls for 16% growth this year, a more than 24-point swing from the 8.2% decline in 2023.

Looking Forward

According to Supplyframe Commodity IQ, many semiconductors are seeing lead time reductions, and apart from memory ICs, just 2% of semiconductor price dimensions are rising in Q3. Passive component and interconnect trends are even more positive, with 83% of lead time metrics showing declines and half of all prices decreasing.

H2 2024 will close with more improvements from a buy-side perspective. Over 90% of pricing dimensions will indicate price flexibility or decreases. Limited assurance of supply concerns will be supported by a 99% share of lead times on the decline or stable.

Even including memory and storage devices in H1 2025 is forecast to be favorable for component procurement teams. Just 8% of lead time dimensions will expand, and 10% of pricing elements will be either rising or inflexible.

But all is not well for the buyer. While lead times will be more stable, order adjustment flexibility will be severely limited. With inventory correction mostly a thing of the past and many component manufacturers operating at a reduced capacity, any sharp demand spikes will result in supply constraints and shortages.

")